Why Banking Malware is Still the Hardest Fraud Problem to Solve in Digital Banking

Banks still treat malware as a security issue to contain. In reality, it remains one of the biggest drivers of digital banking fraud and one of the hardest to detect before the damage is done.

Data shows users encountering mobile banking trojans surged 3.6 times year over year. Malware is scaling fast while controls are still reacting too late. Detection alone won’t cut it.

How Banking Malware Works

Banking malware is a method of malicious software used to extract sensitive financial data (such as login credentials or account numbers), designed to operate inside legitimate banking sessions, often without triggering traditional controls.

How Banking Malware Steals Data

Once malware infects a device or session, it quietly harvests sensitive information using a variety of covert techniques. This includes recording keystrokes, capturing data from web forms before it’s encrypted, taking screenshots when banking apps are opened, or stealing stored passwords and browser cookies.

Many malware strains combine several of these techniques in a single attack. Some go even further, silently altering banking pages during a live session or placing fake screens over mobile apps to trick users into handing over their credentials. By the time the techniques are visible, the session already appears legitimate to traditional detection systems.

Where and How You Get Infected by Malware

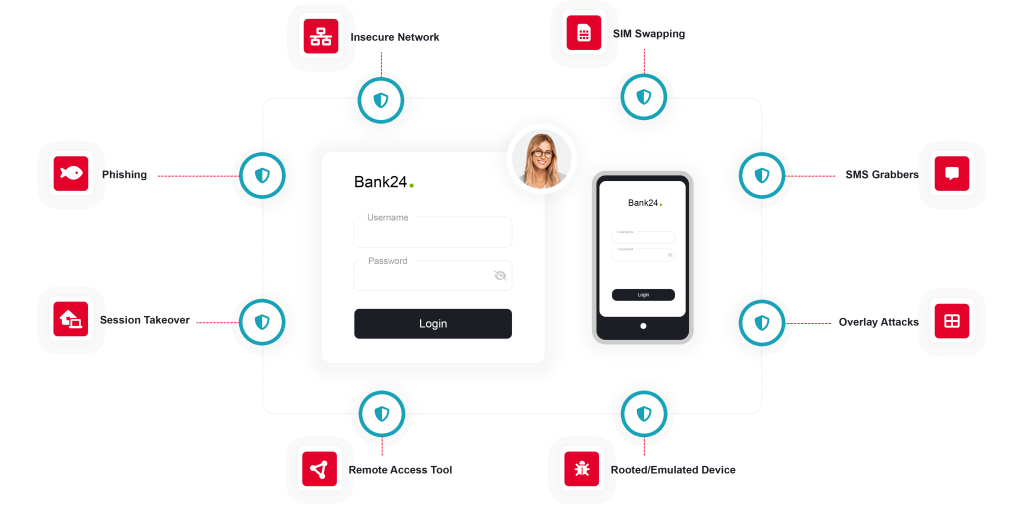

Banking malware doesn’t force its way in. It’s invited in through everyday user behavior. These threats are often hidden in routine activities, making them difficult to spot with the naked eye or catch with traditional antivirus tools.

Phishing Emails and Messages

A classic trick: users receive an email or a text message that looks like it’s from their bank or a trusted provider. One click on a malicious link or attachment, and malware quietly installs in the background, often without any visible sign —which means detection often starts after the device is already compromised.

Malicious Apps

Mobile malware, including banking malware, often hides in apps that appear harmless—like PDF viewers, QR code scanners, or phone cleaners—and sometimes even makes it onto official app stores. Once installed, these apps request excessive permissions, letting attackers capture input, intercept SMS messages, or overlay fake login screens to steal credentials.

Lookalike or Compromised Websites

Cybercriminals clone real banking websites down to the pixel. If a user logs in on one of these fake pages, their credentials are harvested in real time and sometimes injected into the real site to bypass verification.

Malicious Browser Extensions or Injections

Some malware hooks directly into the browser to manipulate how banking pages behave. These “man-in-the-browser” (MitB) attacks can change transaction details, add hidden fields, or capture information before it’s encrypted.

Software Vulnerabilities

Some banking malware doesn’t wait for a click. It exploits unpatched vulnerabilities in browsers, operating systems, or plugins, installing malware silently through drive-by downloads. Just visiting a compromised site or using outdated software can be enough to trigger infection, making these attacks especially dangerous on otherwise trusted devices.

Types of Banking Malware to Know in 2026

Malware targeting banks and their customers comes in many forms. Some focus on stealing login credentials, others aim to take full control of the session, and some go even further, encrypting data or spreading across networks.

The threat landscape shifts quickly. Families are disrupted, rebranded, and rebuilt. The specifics vary, but the patterns don’t: once malware is active inside a session, traditional controls struggle to distinguish fraudulent activity from legitimate.

Here’s what banks should watch closely in 2026.

Banking Trojans

Banking trojans are some of the most common types of financial malware. They often pose as legitimate files or apps, making it easy for users to install them without realizing the danger. Once inside, they quietly steal banking credentials, intercept transactions, or take over browser sessions, usually without the user noticing a thing.

Some of the more prominent banking trojan and loader families in recent years include DanaBot and the Gozi/ISFB lineage, along with IcedID, which is frequently used for initial access. Emotet also remains a persistent threat, operating primarily as a delivery mechanism for follow-on malware. While legacy families like Zeus shaped today’s threat landscape, modern campaigns are increasingly modular, with banking trojans often serving as an initial foothold for broader criminal operations.

Remote Access Trojans (RATs)

Remote Access Trojans, or RATs, give attackers full control of an infected device. Unlike banking trojans that primarily steal credentials, RATs allow fraudsters to view the screen, move the mouse, and initiate transactions just like a legitimate user would.

In banking fraud, RATs are frequently used to bypass authentication controls, approve transfers, and manipulate live sessions in real time. In many cases, victims are socially engineered into installing remote access tools themselves, believing they are granting access to technical support or security staff.

Because RATs operate silently within the user’s device and mimic trusted behavior, they’re especially dangerous and particularly hard to detect without in-session behavioral monitoring. For fraud teams, this is the worst-case scenario: activity that looks indistinguishable from a legitimate user.

Ransomware

Ransomware doesn’t just steal data—it locks it up and demands payment, disrupting operations and exposing organizations to financial and reputational damage. While this threat is typically associated with enterprise-wide disruption rather than session-level banking fraud, its impact on the financial sector remains significant.

Between 2021 and 2024, the share of financial institutions reporting ransomware attacks nearly doubled, from 34% to 65%, according to Security.com. Meanwhile, a survey by Netacea confirmed that ransomware is now viewed as the top cyber threat among businesses in the UK and US.

Despite ransom payments dropping 35% in 2024 to around $813 million, the threat hasn’t gone away. Attackers have adapted with new ransomware strains, faster operations, and tactics that kick off negotiations within hours of stealing data.

Spyware and Infostealers

Spyware and infostealers silently collect sensitive data over time—such as credentials, cookies, and screenshots—without alerting the user. Examples like RedLine, Agent Tesla and Vidar often spread through phishing campaigns or malicious downloads. On mobile devices, banking-focused malware such as TeaBot uses overlay attacks and accessibility abuse to capture credentials and intercept financial data.

Botnets and Automated Attack Infrastructure

Botnets are networks of infected devices controlled remotely to power large-scale attack campaigns. They distribute malware, send phishing emails, and automate credential-stuffing or brute-force attempts against financial institutions and their customers. Modern bot attacks increasingly rely on automation frameworks that mimic legitimate user behavior, making malicious traffic harder to distinguish from genuine activity.

Despite being underestimated—only 11% of organizations named them the top threat, according to Netacea—bot attacks are costly. For large enterprises, annual losses can exceed $85 million, more than fifty typical ransomware payouts. Rather than relying on a single malware family, today’s bot infrastructure often supports a rotating ecosystem of infostealers, loaders, and phishing kits.

Man-in-the-middle Attacks

Man-in-the-middle (MitM) attacks manipulate live banking sessions in real time by intercepting or altering communication between the user and the bank. This can include changing transaction details, injecting fake fields, or capturing authentication codes—often without the user noticing.

MitM techniques are frequently used in advanced phishing kits and can also be enabled by malware that hijacks session data or intercepts one-time passcodes, allowing attackers to bypass traditional protections such as two-factor authentication.

Challenges in Detecting Banking Malware

Modern banking malware is designed to stay invisible until it matters. It evolves rapidly, spreads across networks, and can bypass traditional detection mechanisms.

Artificial intelligence is making things even harder, helping attackers craft smarter phishing lures, generate new code, and automate evasion tactics.

Why Detecting Banking Malware Is So Difficult

Banks face a growing number of challenges when trying to detect banking trojans and malware:

- Traditional security falls short: Antivirus and rule-based systems struggle with polymorphic malware that constantly changes its code. And if the user’s device is already compromised, transaction monitoring alone may not detect manipulation occurring within an active session.

- Evasion techniques are getting smarter: Some malware lies dormant until users access their online banking service. Others hijack sessions and intercept authentication data without leaving obvious traces. More recent Android banking malware has gone a step further by deliberately mimicking human interaction patterns to evade detection.

- AI-assisted malware is now mainstream: Attackers increasingly use AI to generate phishing content, refine malicious code, and automate variation across campaigns, enabling faster iteration and large-scale customization.

- Malware-as-a-Service lowers the bar: Ready-made malware kits enable less-skilled actors to launch advanced attacks, increasing both the volume and variety of threats.

By the time most controls react, the fraudster is already inside the session. The problem isn’t visibility. It’s timing.

Modern Techniques for Advanced Banking Malware Prevention

Stopping malware before it leads to fraud requires detecting threats during the session and disrupting them across the fraud chain. The following techniques help spot risks in real time, protect users in-session, and cut off fraudsters before they can profit.

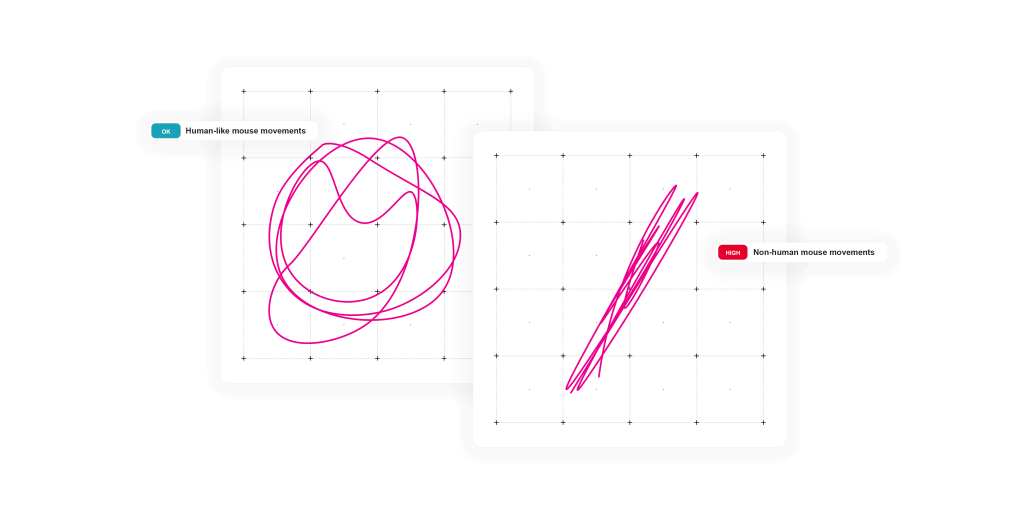

Behavioral Biometrics

Behavioral biometrics focuses on how users behave, not just what they do. Typing rhythm, mouse movement, and touchscreen swipes create subtle patterns that are highly individual and difficult to replicate consistently over time. This becomes critical when malware is already operating in the banking session.

Behavioral intelligence tracks these patterns in real time, comparing each session to the user’s usual behavior. This allows banks to identify meaningful deviations, whether caused by a fraudster, a bot, or malware controlling the session.

Unlike basic bot-detection systems that focus on distinguishing humans from automation, behavioral intelligence analyzes whether the person interacting with the device matches the legitimate user. This means that even malware designed to mimic human behavior—such as the Herodotus Android banking trojan, which introduces randomized input delays—does not automatically evade detection.

The system evaluates consistency, continuity, and contextual shifts across the entire session, allowing banks to surface high-risk anomalies even when the activity appears superficially human and the device itself is trusted.

Early-Warning Threat Detection

Stopping malware after it strikes is too late. By that point, financial loss and customer friction are already in motion. The real goal is to detect threats early—sometimes before they ever reach the customer. By identifying malicious code injections, session anomalies, and fraudulent banking domains, banks can surface risks before financial loss occurs.

Early threat detection extends beyond the session. By working with app stores, search engines, domain registrars, and hosting providers, it helps identify and take down phishing infrastructure, disrupting fraud operations upstream and stopping attacks before they reach customers.

Continuous Monitoring of In-App Behavior

Session-based fraud detection is essential when malware operates post-login. Continuous monitoring tracks the entire session flow—not just the transaction—flagging anomalies such as:

- Unexpected navigation paths

- Form tampering or field injection

- Behavioral inconsistencies in input patterns

- Activity that deviates from the user’s established device or channel profile

This approach helps surface indicators of man-in-the-browser attacks, RAT-controlled sessions, or automated bot attacks, even when the device passes fingerprinting checks and two-factor authentication.

Device Intelligence

Understanding the context of every session is critical, as modern banking malware may operate on emulators, rooted devices, or within spoofed browser sessions that appear legitimate on the surface. Device intelligence adds a crucial layer by identifying subtle signs of risk: unusual OS or browser configurations, tampered environments, or known high-risk device attributes.

It detects indicators of compromise and combines them with behavioral analysis to build a comprehensive risk profile. This layered context helps banks uncover hidden threats early, even when the malware is designed to remain invisible.

Intelligence-Driven Risk Scoring

Signals from user behavior, device integrity, session monitoring, and external threat intelligence are continuously evaluated through real-time risk models. Instead of reacting after fraud occurs, banks can respond dynamically—limiting functionality, requiring step-up authentication, or interrupting high-risk sessions before financial loss happens.

Proactive Prevention Is the New Mandate for Financial Institutions

Banking malware is a constantly evolving threat that intersects with other fraud vectors. It often begins with phishing infrastructure, progresses through device compromise and in-session manipulation, and ends with laundering stolen funds. Preventing losses means intervening across that entire chain.

Fraud Disruption moves defenses beyond point-in-time detection toward coordinated, end-to-end intervention. It connects early signals from phishing domains and malicious infrastructure with real-time session protection and post-transaction intelligence that helps uncover mule networks. By layering these capabilities, banks can reduce exposure before login, intervene during high-risk sessions, and limit fraudsters’ ability to cash out.

Because in the era of modern banking malware, detection alone is no longer enough. By the time detection happens, the damage is done. Disruption is what changes the outcome.

Banking Malware Prevention FAQs

What are the primary types of mobile banking malware we should be concerned about?

The main mobile threats are Android banking trojans that use overlay attacks and accessibility abuse to steal credentials and manipulate transactions. Some include RAT-like remote control capabilities, while mobile infostealers harvest login data and authentication codes. Botnet abuse and mobile ransomware exist but are less common in banking-focused fraud.

How are current malware trends impacting fraud detection strategies?

Modern banking malware is increasingly integrated into broader fraud schemes. As threats become more adaptive and automated, detection strategies must move beyond point-in-time checks toward continuous monitoring, early infrastructure disruption, and coordinated intervention across the fraud lifecycle.

How can we improve our existing malware detection capabilities?

Improving malware detection requires combining device intelligence, continuous behavioral monitoring, and threat intelligence to surface risk in real time—across devices, live sessions, and even post-transaction activity. When integrated into a broader fraud disruption strategy, these capabilities help break the fraud chain before losses occur.

How can we incorporate machine learning and AI into our fraud detection workflows?

Machine learning strengthens fraud detection by identifying behavioral patterns that static rules miss, while AI supports dynamic risk scoring and alert prioritization as fraud tactics evolve. Modern platforms integrate with legacy systems via secure APIs or API-less options, enabling incremental adoption without major infrastructure changes.

What are the emerging technologies that will shape the future of banking malware detection?

Behavioral intelligence and AI-driven risk orchestration will define the next phase of malware detection, enabling earlier intervention and coordinated disruption. At the same time, intelligence sharing between financial institutions will become critical, as fraudsters collaborate at scale and banks must do the same.

Talk to a fraud fighter

Related Articles

-

July 8, 2026

UI Manipulation Fraud: When Users Can No Longer Trust What They See

Fraudsters found a new way around established controls: UI manipulation fraud. By altering information displayed during legitimate banking...

July 8, 2026

UI Manipulation Fraud: When Users Can No Longer Trust What They See

Fraudsters found a new way around established controls: UI manipulation fraud. By altering information displayed during legitimate banking...

-

December 22, 2021

About S.O.V.A. Malware Family

Our SOC team has reverse-engineered the peculiar S.O.V.A malware family. In this article read about the uniqueness of...

December 22, 2021

About S.O.V.A. Malware Family

Our SOC team has reverse-engineered the peculiar S.O.V.A malware family. In this article read about the uniqueness of...

-

May 27, 2021

On Mobile Banking Malware

Last week our SOC experts exposed FluBot – one of the most dangerous mobile banking malware currently in circulation.

Its...

May 27, 2021

On Mobile Banking Malware

Last week our SOC experts exposed FluBot – one of the most dangerous mobile banking malware currently in circulation.

Its...